Woolworths Picked DoorDash, Coles Picked Uber Eats – Why?

Woolworths Picked DoorDash, Coles Picked Uber Eats – Why?

Last Updated on January 2, 2026

Key Takeaway

What You’ll Learn:

- Woolworths and Coles selected delivery platforms to retain control over operations, data, and long-term strategy.

- Aggregator platforms generate demand quickly but reduce direct brand ownership and customer recall.

- Owning customer data strengthens retention, improves margins, and increases long-term business valuation.

- Food delivery platforms perform best when founders control distribution, pricing, and customer relationships.

- Uber Eats-like platforms allow faster market entry with predictable costs and scalable unit economics.

Stats That Matter:

- Uber Eats and DoorDash control over 70% of Australia’s food delivery market.

- Delivery platforms charge up to 35% commission per order.

- Owned platforms improve repeat purchases by up to 30%.

- Platform-led businesses achieve higher valuation multiples.

- White-label platforms reduce launch time by nearly 50%.

Real Insights:

- Platform dependency reduces brand recall over time.

- Owning the app means owning the customer relationship.

- Early niche focus beats broad market competition.

- Simpler platforms launch faster and scale smarter.

- Long-term ROI improves when founders control data and margins.

Woolworths Picked DoorDash, Coles Picked Uber Eats – Why?

Watching grocery giants pick sides in the delivery wars feels a bit like a group chat split you didn’t see coming. One moment, everyone’s riding the same wave. Next, Woolworths goes with DoorDash, and Coles backs Uber Eats. Cue the hot takes. But behind the headlines, this wasn’t a vibes-based decision. It was a calculated platform move.

For CEOs and founders paying attention, this moment matters. These partnerships weren’t about who has more riders or flashier promos. They were about distribution control, customer data ownership, API depth, fulfillment reliability, and long-term margin math. In other words, the stuff that actually decides who wins at scale.

If enterprises with billion-dollar balance sheets are still cautious about platform dependency, early-stage founders should be asking harder questions. Because what looks like “outsourcing delivery” is really a lesson in platform strategy – and why more brands are quietly preparing to own their own food delivery stack.

What Exactly Happened Between Woolworths, Coles, Uber Eats, and DoorDash?

At a surface level, the story looked simple: Australia’s two largest grocery retailers chose different delivery partners. But the reality is more nuanced.

In late 2024, Woolworths announced a partnership with DoorDash, while Coles deepened its alignment with Uber Eats. This immediately raised questions across retail, logistics, and startup circles: why would two similar businesses back competing platforms?

The answer lies in strategy, not scale.

Both Woolworths and Coles already had internal delivery capabilities. These partnerships were not about “starting delivery.” They were about extending reach without surrendering operational control. Each retailer evaluated platform strengths differently – based on geography, customer behavior, fulfillment models, and integration depth.

In Australia, more than 70% of online food delivery transactions already flow through just two platforms, making dependency a structural risk rather than a short-term trade-off.

This wasn’t a bet on who delivers groceries faster.

It was a decision about how much of the customer journey each brand was willing to outsource.

Is One Platform Actually Better – or Is This the Wrong Question to Ask?

Founders often ask, “Which platform should I choose?”

Large brands ask a different question: “What am I giving up by choosing any platform?”

Neither Uber Eats nor DoorDash is objectively “better” in all scenarios. Each operates with a different marketplace DNA.

What mattered to Woolworths and Coles was not app downloads or rider counts. It was:

- Who controls the customer data?

- Who owns demand signals and repeat behavior?

- How flexible is the integration layer (APIs, order orchestration, logistics routing)?

- How predictable are margins at scale?

Who Really Owns the Customer When You Use a Delivery Platform?

When brands operate inside aggregator ecosystems, the platform typically owns:

- Customer profiles

- Behavioral data

- Recommendation logic

- Promotional visibility

The brand fulfills the order, but the platform owns the relationship.

Large retailers accept this trade-off selectively and temporarily. Early-stage founders often accept it blindly and permanently.

Why Do Large Brands Accept High Commissions in the Short Term?

Because they understand sequencing.

For enterprises, platforms are used to:

- Accelerate market penetration

- Test delivery economics

- Capture incremental demand

But long-term value is created outside the aggregator. That’s why major brands rarely rely on a single platform – and never design their future around one.

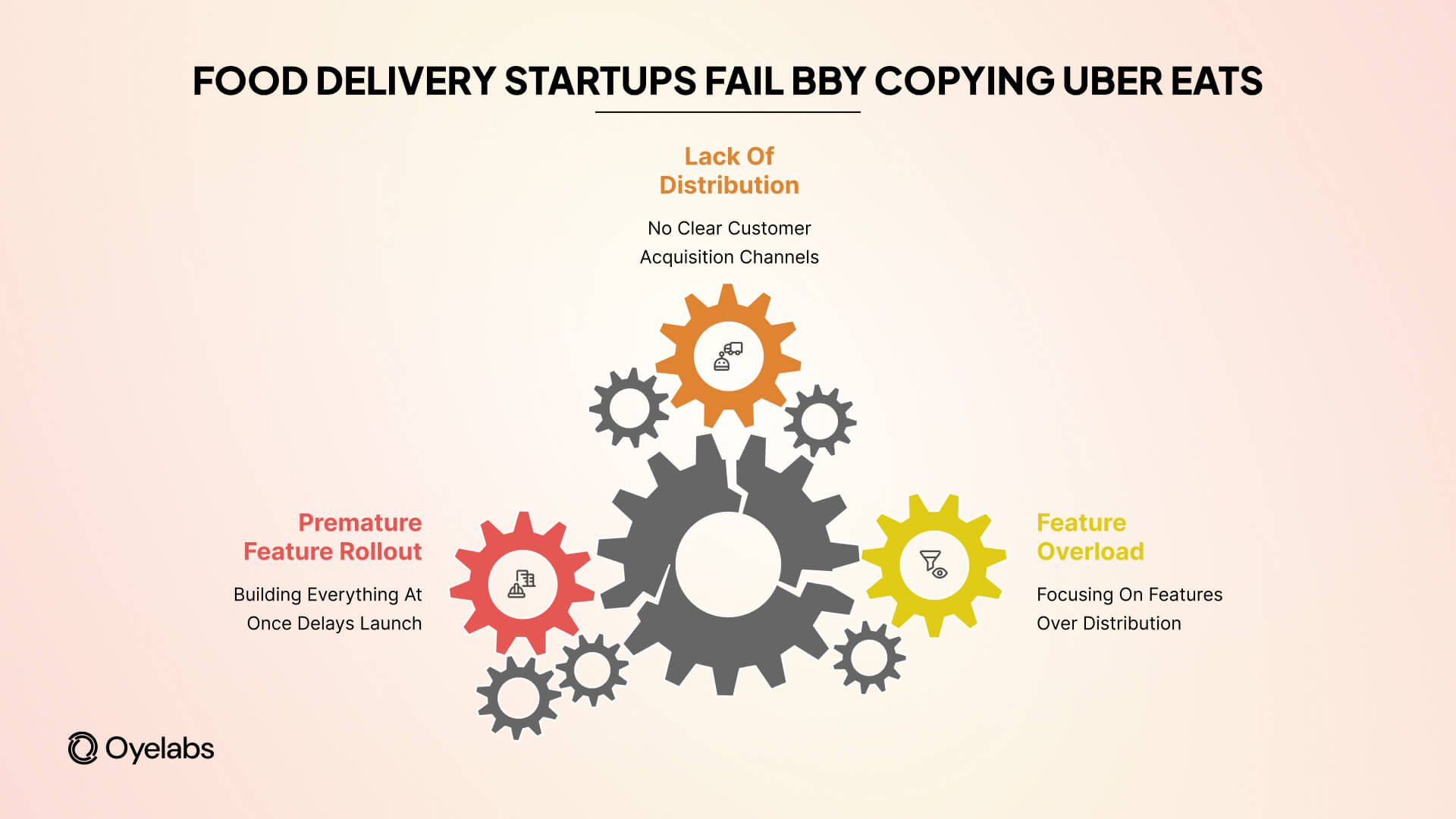

What Do Founders Commonly Misunderstand When They Try to Copy Uber Eats?

Many startups assume that building a food delivery business means copying Uber Eats feature-for-feature. This is one of the most expensive mistakes early founders make.

Uber Eats is not a product.

It is a distribution machine built over years, supported by massive capital, logistics density, and behavioral data.

Are Features Enough to Win a Food Delivery Market?

No. Features are table stakes.

What actually determines success:

- Local supply density

- Operational reliability

- Clear niche positioning

- Direct customer acquisition channels

An app with 100 features but no distribution is still invisible.

Should You Build Everything at Once – or Launch in Stages?

Winning platforms are built in layers, not in one launch.

Successful founders prioritize:

- Ordering and payments first

- Vendor onboarding second

- Logistics integrations third

- Loyalty, subscriptions, and growth loops later

Trying to match Uber Eats on day one usually leads to delayed launches, bloated budgets, and unclear market fit.

The smarter approach is to build ownership early, then expand deliberately – something large retailers already understand and startups must learn faster.

Why Should This Decision Make Startup Founders Pay Attention Right Now?

When companies the size of Woolworths and Coles hesitate to place all their bets on a single delivery platform, it sends a clear signal to founders: platform dependency is a risk, not a shortcut.

These retailers have scale, bargaining power, and internal logistics teams – yet they still diversified their platform exposure. That alone should prompt early-stage founders to pause before committing their entire growth strategy to one aggregator.

The lesson here is not “don’t use Uber Eats or DoorDash.”

The lesson is don’t let them define your future.

If Woolworths Didn’t Commit to One Platform, Should You?

Large brands treat aggregators as channels, not foundations. They test, learn, negotiate, and retain optionality. Startups often do the opposite – building their entire customer funnel inside someone else’s ecosystem.

That creates three long-term problems:

- No control over pricing or promotions

- Limited access to customer data

- Zero leverage when commissions increase

By the time founders realize this, switching costs are already high.

What Is the Hidden Cost of “Easy Growth” Through Aggregators?

Aggregator-led growth feels fast, but it comes with invisible trade-offs:

- Your brand becomes secondary to the platform brand

- Repeat customers remember the app, not you

- Margins tighten as volume grows

This is why experienced operators see aggregator growth as temporary acceleration, not a sustainable moat.

Are Big Brands Quietly Moving Away From Aggregators?

Yes – but not loudly, and not overnight.

Most large retailers won’t publicly announce an “exit” from platforms like Uber Eats or DoorDash. Instead, they slowly rebalance toward owned ordering experiences, private delivery networks, and first-party data systems.

Why Are More Companies Building Their Own Ordering Platforms?

Owning the platform changes the economics entirely:

- Full visibility into customer behavior

- Direct control over loyalty and pricing

- Freedom to experiment without algorithm constraints

Aggregators are excellent at demand aggregation. They are not designed to help brands build long-term equity.

This is why many companies now run a dual strategy: aggregators for reach, owned platforms for retention.

Is This Shift Limited to Grocery – or Spreading to Other Industries?

Grocery is just the most visible example.

The same shift is happening across:

- Restaurant chains

- Cloud kitchens

- Local food brands

- Subscription meal services

Anywhere margins matter and repeat behavior drives value, platform ownership becomes inevitable.

What Don’t Uber Eats and DoorDash Want Brands to Think About?

Aggregators position themselves as growth partners – and in the early stages, that’s true. But their incentives are not aligned with brand independence.

Platforms optimize for:

- Order frequency

- Basket expansion

- Platform stickiness

Brands optimize for:

- Loyalty

- Margin stability

- Long-term customer value

These goals eventually diverge.

What Happens When a Platform Becomes Bigger Than Your Brand?

At scale, brands face:

- Reduced visibility unless they pay more

- Algorithm-driven demand volatility

- Limited negotiation power

At that point, growth slows – not because demand drops, but because control is lost.

Is Long-Term Independence Always the End Goal?

For most serious founders, yes.

The most resilient businesses use aggregators to learn fast, then transition customers to owned platforms where relationships, data, and margins are protected.

That transition is easier when planned early – and extremely difficult when ignored.

Can Startups Really Launch Their Own Food Delivery Platform Today?

Five years ago, the answer would have been “only with deep pockets.” Today, the answer is more practical – and more encouraging.

Technology, infrastructure, and consumer behavior have matured. Payments, maps, notifications, and logistics APIs are no longer experimental. What once required years of engineering can now be assembled intelligently, provided founders focus on strategy before scale.

The real barrier is no longer technology.

It’s clarity.

Do You Need to Compete With Uber Eats – or Just Own a Niche?

Founders don’t lose because Uber Eats exists. They lose because they try to compete head-on instead of positioning precisely.

Winning platforms usually start with:

- A defined geography (one city or region)

- A clear supply focus (local restaurants, cloud kitchens, specialty food)

- A specific customer promise (speed, quality, pricing, community)

Owning a narrow market deeply is far more effective than chasing national scale too early.

How Do You Control Distribution Without Burning Cash?

Modern delivery platforms don’t rely on a single channel. Smart founders combine:

- Native apps for loyal users

- Progressive web apps for fast access

- Direct links, QR ordering, and repeat flows

- Organic and community-driven acquisition

This approach reduces dependency on paid acquisition while building direct customer habits – something aggregators are structurally not designed to support.

What Happens When a Founder Stops Relying on Aggregators and Builds Their Own Platform?

One founder Oyelabs worked with entered the market heavily dependent on third-party delivery apps. Orders were steady, but margins were thin, customer recall was weak, and brand visibility was limited.

Instead of fighting the platforms, the founder launched an owned food delivery platform – similar in experience to Uber Eats, but tailored to a specific regional audience. Over time, customers began ordering directly. Engagement increased, repeat behavior improved, and the brand’s perception shifted from “another restaurant on an app” to a standalone platform.

That shift had a compounding effect: stronger customer loyalty, higher impressions across digital channels, and a noticeable lift in market value. The business didn’t just process orders anymore – it became a brand. Execution support came from Oyelabs, but the outcome was driven by ownership, not technology alone.

Is Building a White-Label Food Delivery Platform Smarter Than Custom Development?

For most early-stage and growth-stage founders, the answer is yes – if the goal is speed with control.

Custom development offers flexibility, but it also brings:

- Longer timelines

- Higher upfront costs

- Uncertain outcomes during early market testing

White-label platforms, when done right, remove unnecessary risk.

How Do Time, Cost, and Risk Compare in 2025?

White-label execution allows founders to:

- Launch faster

- Validate markets earlier

- Allocate budget toward growth instead of rebuilding basics

The strategic advantage is not cutting corners – it’s cutting delay.

What Features Actually Matter in a Food Delivery MVP?

Most successful MVPs focus on:

- Clean ordering and checkout

- Reliable payments

- Simple vendor onboarding

- Clear order tracking

- Actionable admin visibility

Everything else – loyalty, subscriptions, advanced analytics – can follow once real usage data exists.

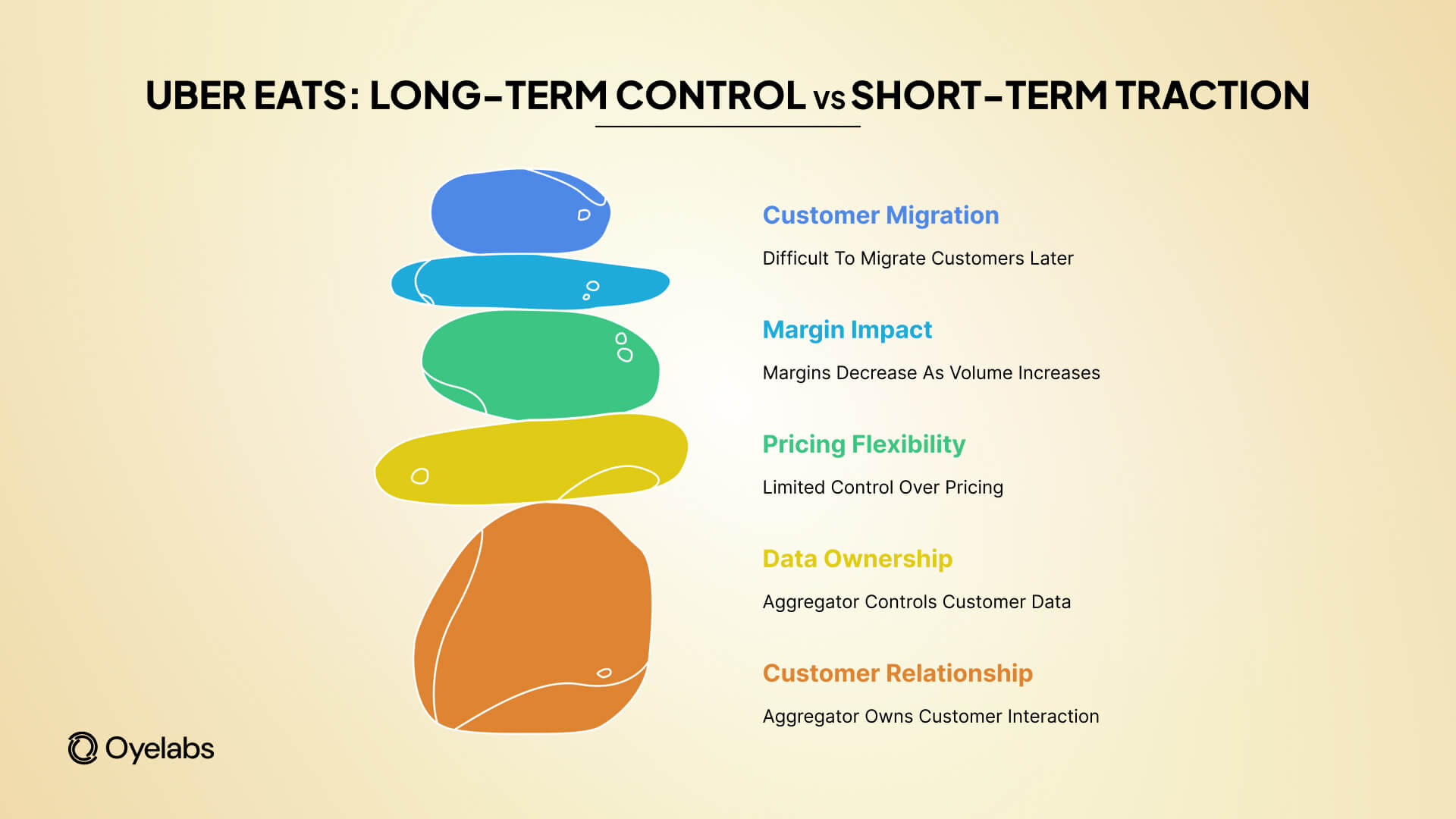

What Should CEOs Ask Before Choosing Uber Eats Over Their Own Platform?

Before committing to any delivery aggregator, experienced CEOs pause and ask questions that go beyond convenience. The goal is not short-term traction, but long-term control.

The most important questions are not technical – they are strategic:

- Who owns the customer relationship once the order is placed?

- Where does customer data live, and who can act on it?

- How much pricing flexibility do we truly have?

- What happens to margins as order volume increases?

- Can we migrate customers later without friction?

If these questions don’t have clear answers, the business is not choosing a delivery partner – it is choosing a dependency.

Aggregators make sense when they accelerate learning. They become risky when they replace ownership. The difference lies in intent, not execution.

What Is the Real Lesson From Woolworths and Coles for Startup Founders?

The takeaway from Woolworths and Coles is not about DoorDash versus Uber Eats. It is about optionality.

Both retailers used platforms to extend reach, but neither surrendered strategic control. They structured partnerships in a way that preserved flexibility, data access, and exit paths.

For startup founders, the parallel is clear:

- Use aggregators to enter the market

- Learn customer behavior quickly

- Build parallel systems that you control

The mistake is not using platforms. The mistake is assuming they are the endgame.

When Should Aggregators Be a Tool – Not a Crutch?

Aggregators work best when:

- They supplement demand, not define it

- They operate alongside owned channels

- They are part of a transition plan

Founders who plan this early move faster later. Those who don’t often find themselves locked into economics they never intended.

Final Thought

The decisions made by Woolworths and Coles reflect a broader shift. Platforms are no longer operational conveniences. They are strategic assets that shape brand power, customer loyalty, and long-term valuation.

For founders and CEOs, the real question is no longer whether delivery should be outsourced. It is whether the customer relationship should be.

Owning a platform does not mean rejecting aggregators entirely. It means designing a future where growth, data, and brand equity remain under your control.

This is exactly where Oyelabs works with founders, not to compete blindly with Uber Eats or DoorDash, but to help them launch owned platforms faster, smarter, and with a clear path to independence.

Because the brands that win tomorrow won’t just list on platforms.

They’ll own the one their customers come back to.

FAQs

Question: Why did Woolworths choose DoorDash while Coles chose Uber Eats?

Answer: Each brand prioritized different distribution, data access, and fulfillment strategies for their target customers.

Question: Is it better to use Uber Eats or build your own food delivery app?

Answer: Using platforms helps early growth, but owning your app protects margins and customer relationships.

Question: Can startups realistically launch an UberEats-like food delivery platform?

Answer: Yes, modern white-label solutions enable faster launches with controlled cost and scalable architecture.

Question: What is the biggest risk of relying only on food delivery aggregators?

Answer: Brands lose pricing control, customer data, and long-term leverage as platforms grow stronger.