AI in Banking – Benefits, Best & Worst Use Cases, & Examples

AI in Banking – Benefits, Best & Worst Use Cases, & Examples

Last Updated on February 4, 2025

AI is making a big impact in banking, and it’s only getting bigger. Financial institutions are increasingly using AI solutions in banking to automate tasks, reduce costs, and improve productivity. As AI technologies become more common, banks are using them to improve many areas, such as fraud detection, loan approvals, and marketing strategies. Sameer Gupta from EY notes that AI is being used in almost every part of banking today, with machine learning (ML) already playing a significant role.

Now, banks are moving beyond basic AI and using more advanced tools like natural language processing (NLP) and generative AI (GenAI). These technologies are helping banks streamline credit approvals, enhance fraud detection, and improve decision-making.

According to Gartner’s Jasleen Kaur Sindhu, in 2024, 42% of banking CIOs have already implemented or plan to deploy AI initiatives, and this number is expected to rise to 77% by 2025. This shows that AI is becoming essential for banks, not just for improving efficiency, but for driving value and success. AI is quickly becoming a core part of how banks operate and serve their customers.

Today, let’s explore how AI is changing the banking sector by looking at its benefits, the best and worst use cases, and real-world examples that highlight its potential.

The Impact of AI in Banking

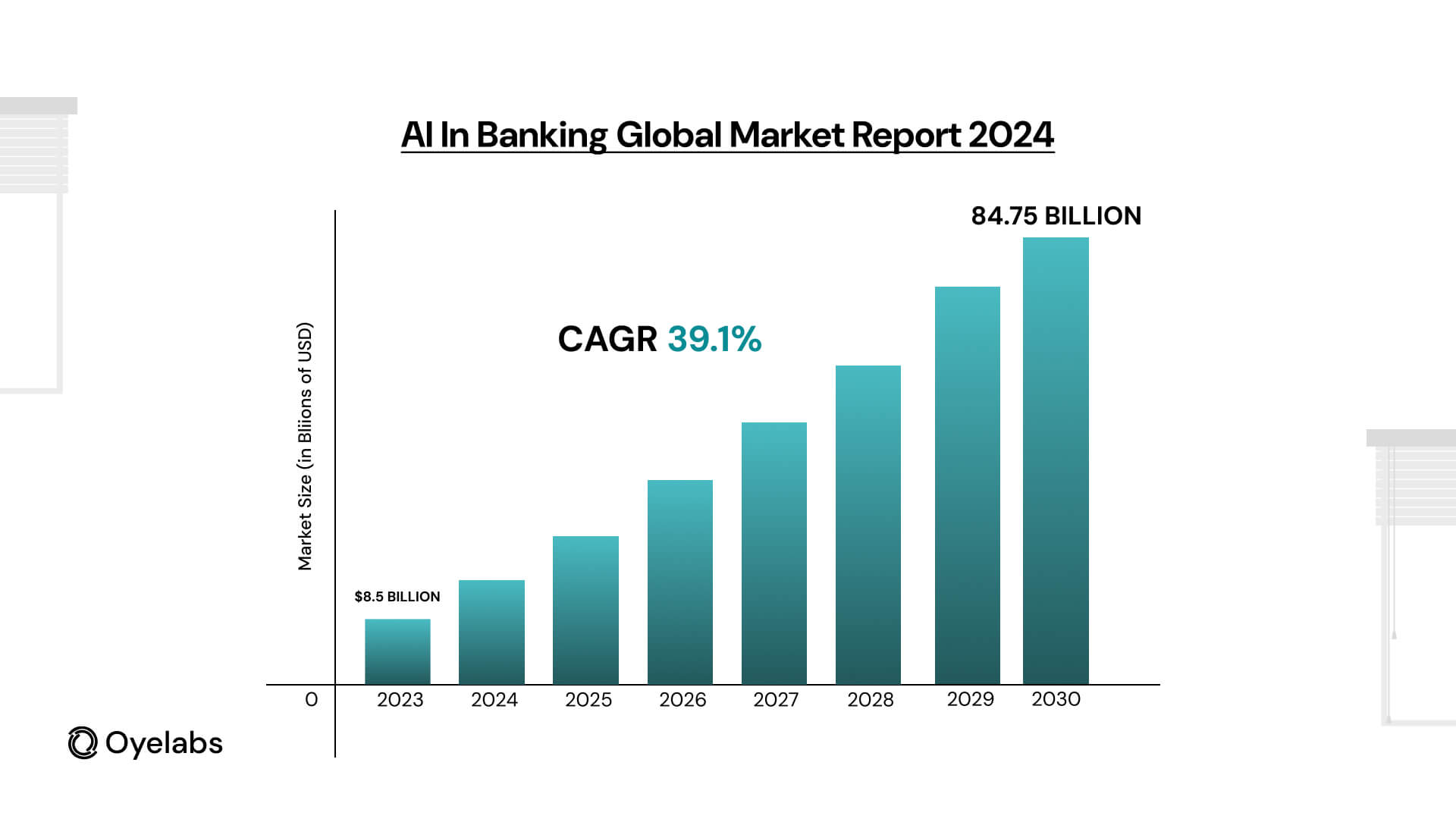

The AI in banking market is expected to grow to $64.03 billion by 2030, highlighting how crucial AI has become to the future of the sector. One of the main areas where AI is making a significant impact is fraud detection. AI-powered systems can analyze transactions in real-time, detecting unusual patterns that may indicate fraudulent activities. By 2025, AI-driven fraud detection could help banks save up to $24.8 billion in global losses, making it a vital tool for reducing financial risks.

In addition to security, AI is improving customer service in banking. Many banks are now using AI chatbots to handle simple inquiries, such as checking account balances or resetting passwords. This allows human agents to focus on more complex issues. With AI handling 85% of customer interactions, it’s clear that it’s becoming an essential part of customer service operations.

AI is also playing a key role in personalizing services for customers. By analyzing vast amounts of data, AI can predict what a customer might need, such as recommending specific financial products or providing tailored advice. This personalized approach helps banks increase customer satisfaction and even boost their revenues by 10-15%.

Moreover, AI is streamlining compliance processes by helping banks keep up with changing regulations. AI can analyze large sets of regulatory data, ensuring that banks comply with laws without overburdening their compliance teams. This has resulted in a 15% reduction in regulatory costs for some institutions.

On the operational side, AI is automating tasks like data entry, document verification, and loan processing, making back-office operations faster and more efficient. Studies show that AI can speed up loan processing by up to 30%, significantly reducing the time and resources needed.

As AI continues to evolve, its role in enhancing security, customer service, personalization, and operational efficiency is becoming increasingly clear.

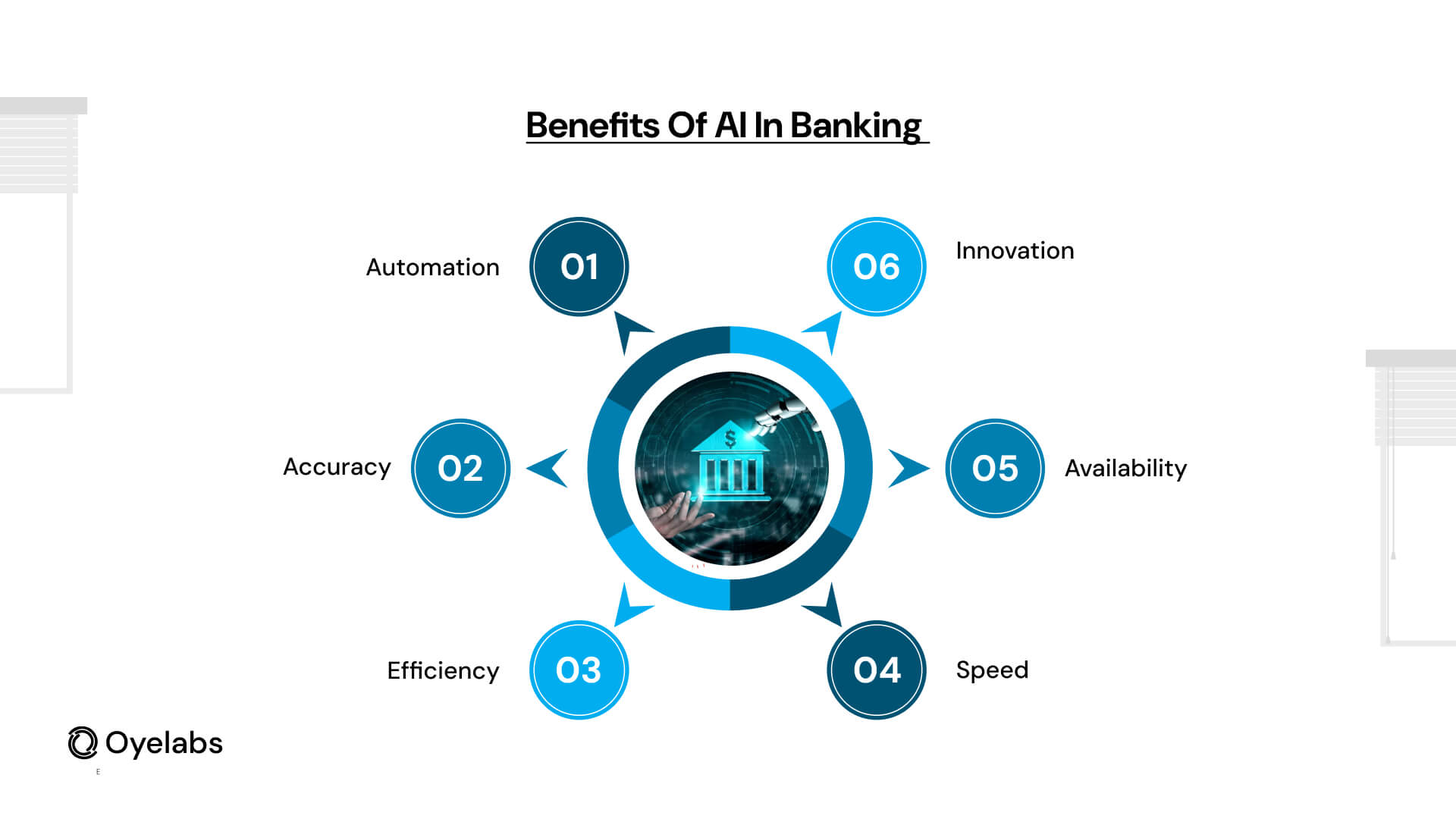

Benefits of AI in Banking

The integration of AI into banking operations offers numerous benefits that significantly improve overall efficiency, accuracy, and service delivery.

Automation

One of the most significant advantages of AI is its ability to automate repetitive and time-consuming tasks. This allows employees to focus on more value-added activities, improving overall productivity. For example, AI systems can automate the document verification process during loan approvals, reducing the time required for manual processing and accelerating decision-making.

AI is also instrumental in enhancing cybersecurity efforts. Machine learning models continuously monitor network traffic, identifying potential threats in real time. These systems can neutralize risks before they escalate into serious security breaches, protecting both bank systems and customer data.

Accuracy

AI improves the accuracy of data processing, reducing human error. With the ability to analyze vast amounts of data quickly and consistently, AI systems can perform tasks such as credit scoring, financial analysis, and fraud detection with a high degree of accuracy. For instance, during customer onboarding, AI ensures that documents are processed and verified without errors, minimizing mistakes that could lead to compliance issues or security risks.

Efficiency

By automating routine tasks, AI enables banks to utilize human resources more effectively. Employees can concentrate on tasks that require creativity, critical thinking, or customer engagement, such as strategic decision-making, managing client relationships, or developing new financial products. This shift from mundane tasks to strategic activities enhances the overall efficiency of the bank.

Additionally, AI-driven customer support allows banks to meet customers’ needs promptly, improving satisfaction and loyalty. In 2023, the main benefit of AI in financial services was the creation of operational efficiencies, with 43% of respondents indicating this advantage.

Speed

AI accelerates decision-making and data processing, which is particularly useful in high-stakes environments like trading. In stock market trading, for example, AI algorithms can process vast amounts of market data in milliseconds, enabling traders to execute trades at optimal times. This capability allows banks to capitalize on fleeting opportunities that would otherwise be missed.

Availability

AI-powered tools, like chatbots, offer 24/7 customer support, ensuring that clients can access assistance whenever needed. Whether it’s checking an account balance, making a transaction, or seeking advice, AI enables banks to provide continuous, real-time service, improving the overall customer experience and satisfaction.

Innovation

AI fosters innovation in banking by enabling banks to analyze vast amounts of data and gain insights that would be impossible to obtain manually. For example, AI systems can identify trends and patterns that lead to the development of innovative financial products, such as personalized investment portfolios, dynamic loan terms, and automated financial management tools. By leveraging these insights, banks can stay ahead of the competition and meet the evolving needs of their customers.

Best Use Cases of AI in Banking

Fraud Detection

AI is a game-changer in detecting fraud. It analyzes transaction data in real time and spots unusual patterns that might suggest fraud. For example, if a customer’s credit card is used in a different city, AI can flag the transaction and notify the customer right away. This system continuously improves itself over time, learning from previous fraud cases. This helps banks reduce fraud significantly. In fact, AI-driven fraud detection has already saved the banking industry billions annually.

Customer Service

AI is revolutionizing how banks serve their customers. Many banks now use AI chatbots to handle common tasks, such as checking balances or resetting passwords.For example, Bank of America’s AI assistant, Erica, can help users manage their accounts, track spending, pay bills, and offer financial advice. With AI handling simple tasks, human agents are freed up to address more complex issues, ensuring faster and more efficient customer service. According to Accenture, 68% of consumers prefer using chatbots for simple banking services, showcasing the increasing popularity and efficiency of AI in customer service.

Loan Processing

AI speeds up the loan approval process by analyzing creditworthiness in real time. Traditionally, loan approvals could take weeks, but AI can process applications in hours. AI uses data from a variety of sources to assess an applicant’s financial history and predict their ability to repay. This quicker decision-making is especially useful in consumer lending, where speed is essential. According to a report by McKinsey, AI has cut loan processing times by over 50% in some banks.

Personalized Financial Advice

AI can help customers make smarter financial decisions by providing tailored advice. It does this by analyzing spending patterns and financial goals. For example, AI might suggest a savings plan that fits a customer’s income and spending habits or offer investment opportunities based on their risk tolerance. This level of personalization is becoming increasingly popular, with 70% of consumers expecting more tailored financial services from their banks by 2025.

Risk Management

AI helps banks better assess and manage financial risks. Using advanced algorithms, AI can analyze financial data and predict potential risks, such as market volatility or credit defaults. This helps banks make more informed decisions about investments, loans, and insurance. AI in risk management is becoming increasingly important, as it enables banks to predict risks faster and more accurately. In fact, AI-powered risk management tools have improved banks’ decision-making efficiency by up to 40%.

Algorithmic Trading

AI is also used in trading, where algorithms analyze vast amounts of market data and execute trades within milliseconds. These AI systems are designed to identify patterns in the market and make decisions on buying or selling much faster than human traders, enabling banks to capitalize on short-term price movements. The speed and precision of AI-powered trading systems have made them indispensable for financial institutions looking to gain a competitive edge. AI algorithms can process data from multiple sources, including news, social media, and market trends, to predict market shifts accurately.

In 2024, 70% of global stock market trades are estimated to be powered by AI-driven algorithms, underlining their growing impact on financial markets. This shift towards AI in trading is not only enhancing trading efficiency but also reducing risks by making real-time, data-driven decisions.

Also Read: Use Cases AI in Transportation

Worst Use Cases of AI in Banking

Bias in Algorithms

AI systems can inherit biases from the data they are trained on. If historical data has biases—such as unequal access to loans for certain demographic groups—AI can continue and even amplify these biases. This can lead to unfair outcomes, like discrimination in loan approvals. For example, a 2019 study found that AI-driven systems used by some financial institutions were more likely to deny credit to minority applicants, even when their financial profiles were similar to others.

Over-Reliance on AI

While AI can improve banking operations, depending too much on it can be risky. If an AI system fails or encounters an error, it can disrupt key services, such as fraud detection or customer support. For example, if a fraud detection system falsely flags a legitimate transaction as fraudulent, it could cause inconvenience for customers. In 2023, nearly 30% of financial institutions experienced downtime due to AI system errors, underlining the importance of human oversight.

Privacy Concerns

AI relies on vast amounts of customer data to function. This raises concerns about privacy and data security. Banks must ensure they have strong security measures in place to protect sensitive information and comply with regulations like GDPR. In 2023, a survey showed that 60% of consumers were concerned about how banks use their personal data, highlighting the need for banks to be transparent about their AI practices.

Errors in Complex Tasks

Although AI excels at repetitive tasks, it struggles with complex situations that require human judgment. For example, AI may not always resolve customer disputes accurately or interpret complex regulatory rules. In these cases, human intervention is still essential. A 2022 report revealed that 25% of AI systems in banking failed to handle customer complaints effectively, stressing the need for human oversight in complicated matters.

Lack of Transparency

One major challenge with AI is its “black-box” nature. Many AI algorithms produce results without explaining how they reached those conclusions. This lack of transparency can lead to problems such as unfair decisions in credit scoring or insurance pricing. In fact, a 2023 study found that 40% of consumers felt uncomfortable with AI decision-making because they didn’t understand how it worked, making transparency a critical issue.

Limited Features

While AI has many impressive capabilities, it is still limited in certain areas. For example, AI systems in banking may struggle to handle tasks that require deep emotional intelligence or nuanced judgment. Complex customer interactions, like understanding personal financial goals in detail or addressing emotional concerns, are areas where AI falls short. Additionally, AI systems are often tailored to specific tasks, meaning they may not adapt well to new or unexpected challenges. This limitation can prevent AI from fully replacing human interaction, particularly in areas that require a personal touch.

In fact, research from Customerzone found that 40% of consumers still prefer speaking to human agents for sensitive matters, illustrating that AI’s features are not yet comprehensive enough to meet all customer needs.

Real-World Examples of AI in Banking

Many leading banks around the world have already implemented AI technology with great success, showcasing its transformative potential for the industry. Here are some notable examples:

JP Morgan: JP Morgan’s COiN (Contract Intelligence) is a cutting-edge AI tool that reviews legal documents. This tool has dramatically reduced the time spent by lawyers and analysts on reviewing documents, saving the bank an estimated 360,000 hours of work annually. The AI system scans and processes documents faster and more accurately than human workers, making legal reviews more efficient. This also allows the bank to streamline its operations, freeing up human resources to focus on more strategic tasks.

HSBC: HSBC uses AI-powered fraud detection systems to detect suspicious transactions in real-time. The AI analyzes transaction data for patterns that may suggest fraudulent activity, helping the bank spot potential fraud before it causes significant damage. This system has been instrumental in reducing fraud-related losses and enhancing the bank’s ability to respond quickly to fraudulent activities, offering better protection for customers’ accounts and improving overall security.

Wells Fargo: Wells Fargo has implemented AI-driven chatbots that provide customers with instant support. The AI chatbot can handle a wide range of queries, from simple balance inquiries to more complex requests, ensuring customers can get help any time of day. This technology has not only improved customer service by offering round-the-clock assistance, but it has also increased operational efficiency, as human agents can now focus on more complicated issues. This integration of AI into customer service shows how banks are enhancing the customer experience through technology.

BBVA: BBVA, a global financial group, leverages AI to offer personalized financial advice to its customers. The AI system analyzes each customer’s financial data, including spending habits, income, and savings, to offer tailored financial recommendations. This can include suggestions for saving money, investing in certain products, or even adjusting spending patterns based on long-term financial goals. By using AI to personalize financial advice, BBVA helps customers make smarter financial decisions, creating a more engaging and customized banking experience.

Also Read: Real-World Applications of AI in Manufacturing

Oyelabs’ AI Solutions

At Oyelabs, we offer AI solutions designed to help banks solve key challenges. Our fraud detection systems monitor transactions in real time, quickly spotting and preventing fraud to protect your customers. With our AI chatbots, your bank can offer 24/7 customer support, handling common tasks like balance checks and money transfers, making customer service faster and more efficient.

Our risk analysis tools use AI to help banks predict and manage risks, improving decisions around investments and loans. We also provide custom AI development, creating solutions tailored to your bank’s needs. Want to improve your banking operations with AI? Contact Oyelabs today to discover how our solutions can help your business grow.

conclusion

The impact of AI on banking is undeniable, offering solutions that improve security, customer service, and operational efficiency. From detecting fraud to offering personalized advice, AI is streamlining key processes across the industry. While challenges like privacy concerns remain, the potential for AI to reduce costs, enhance services, and boost revenue makes it a must-have tool for banks looking to thrive in the digital age.

Adopting AI is no longer optional for banks—it’s essential. If you want to stay ahead in the competitive banking industry, let Oyelabs show you how AI can take your operations to the next level. Reach out today and start your journey toward smarter banking solutions.

Also Read: AI in Food Industry